Envela’s Venture Into Electronics Re-Commerce Is Paying Off

Galeanu Mihai

Introduction

I like writing about undercovered shares on SA, and today I am using a appear at Envela Company (NYSE:ELA). It really is a re-commerce retailer that has additional than tripled its product sales given that 2016 and appears established to ebook a net profits of above $10 million for 2022. The company has a current market capitalization of practically $200 million as of the time of composing, but I feel it really is affordable thinking about how prosperous its turnaround has been many thanks to the undertaking into electronics. Let’s critique.

Overview of the enterprise and financials

Envela was launched in 1965 and is among the the most significant authenticated re-commerce suppliers of luxurious hard assets in the United states. The company’s small business is break up in two operating segments. Its DGSE subsidiary is involved in the obtain, and re-sale or recycling of jewelry, diamonds, gemstones, wonderful watches, uncommon coins, gold, and silver and it has a network of 7 jewellery shops throughout the state of Texas and South Carolina. Its makes involve Dallas Gold & Silver Exchange, Charleston Gold & Diamond Exchange, and Bullion Specific. Envela’s ECHG subsidiary, in change, specializes in the buy and recycling or refurbishment of purchaser electronics and IT products. This segment generates revenues through re-offering, end-of-everyday living electronics recycling, and IT property disposition providers. ECHG aims to extend the handy life of electronics as a result of re-commerce each time probable, and it recycles products as a result of the removal of usable parts for re-sale as parts, or by extracting the worthwhile metals.

Envela

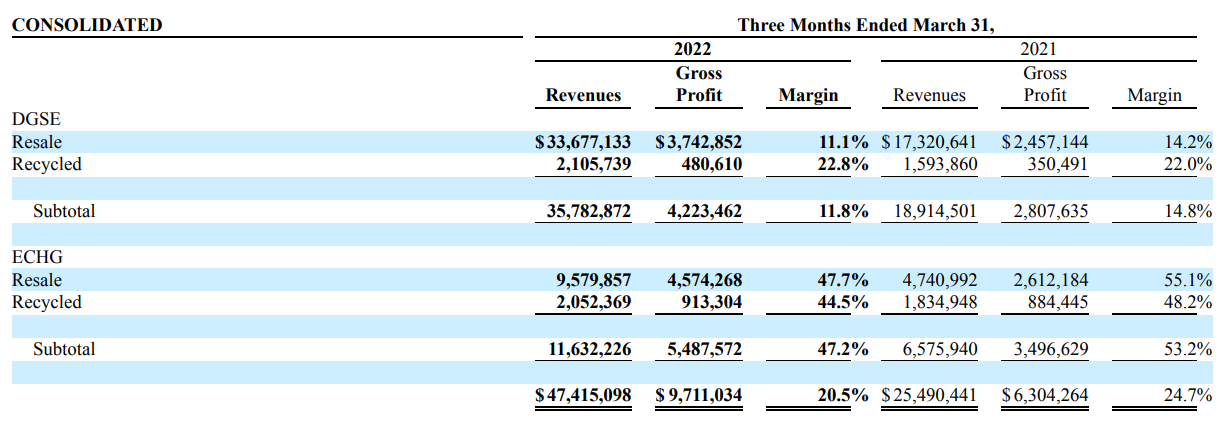

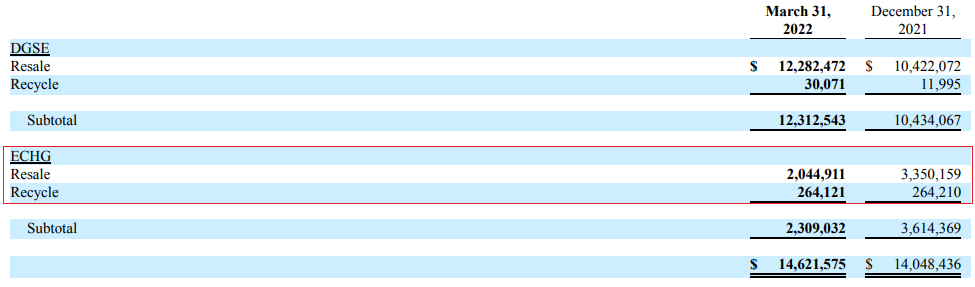

On the lookout at the newest accessible financials of Envela, we can see that the vast bulk of the firm’s revenues are coming from re-promoting and not recycling and that ECHG has much improved margins than DGSE.

Envela

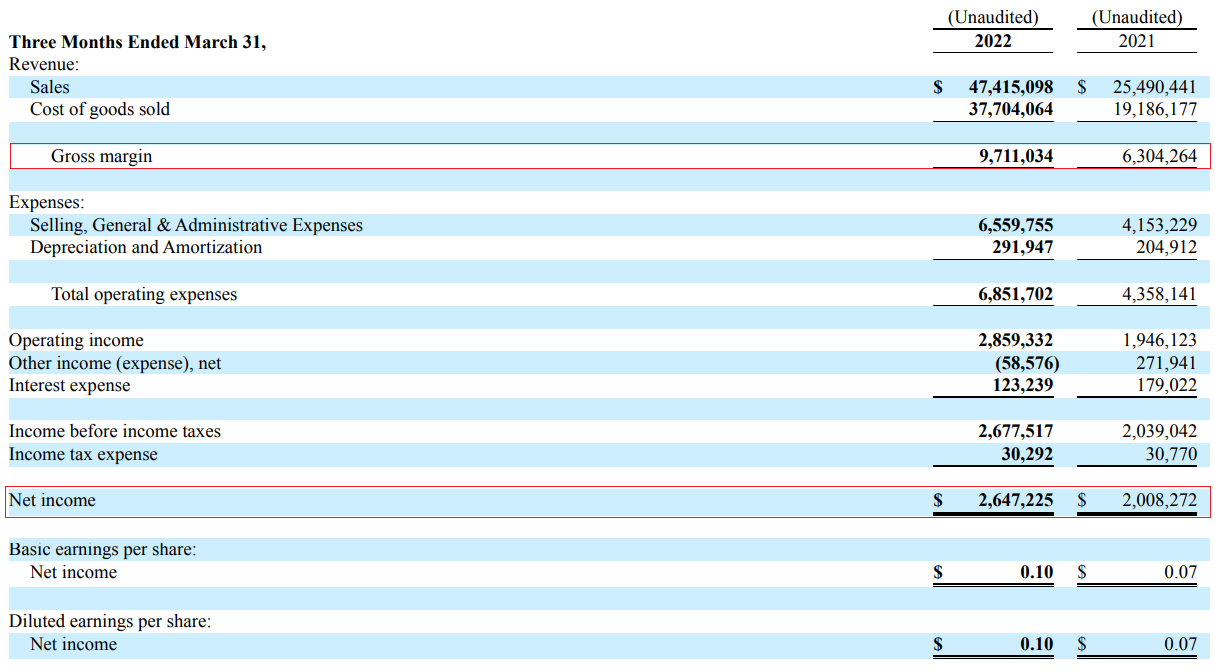

You can also see that the revenues of both of those segments registered sizeable expansion in Q1 2022. DGSE’s embarked on an on-line advertising and marketing and advertising marketing campaign during the interval and boosted its promoting spending plan by 56%. It appears to be the internet marketing marketing campaign was effective. I imagine the increase in ECHG’s revenues, in switch, can be attributed to the order of two enterprises in 2021. In June 2021, Envela bought electronics trade-in and recycling support company CExchange. In October, the organization obtained IT asset disposition expert services company Avail. General, I think Q1 2022 was a quite strong period from a economic issue of see for Envela as the gross gain soared by 54% to $9.7 million while the net earnings rose by almost 32% to $2.7 million. In my perspective, the enterprise is probably to ebook a net profits of about $10 million for 2022.

Envela

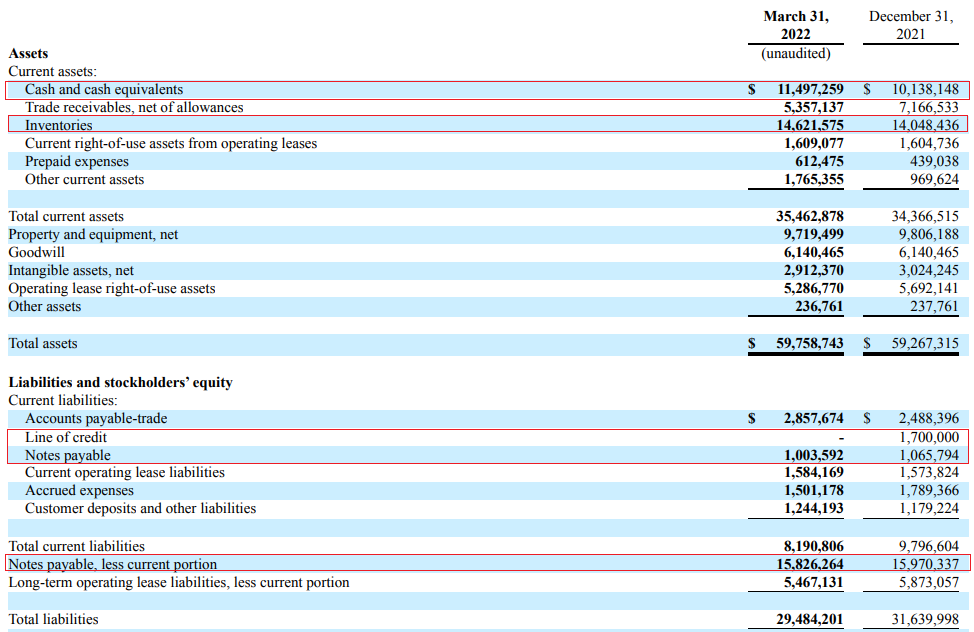

Turning our awareness to the stability sheet, we can see that Envela has a relatively asset-mild small business with money and inventories accounting for pretty much 50 % of the asset base as of March 2022. Credit card debt stood at $16.8 million at the conclude of the quarter, which I believe is effortlessly manageable thinking of income and money equivalents had been $11.5 million. In addition, capital expenses are expected to be just all around $1 million more than the coming 12 months. In my perspective, Envela has plenty of liquidity to finance a single or two more acquisitions in the near long run.

Envela

Envela seems overvalued at 1st glance, as it has a current market valuation of $197.1 million as of the time of creating. The company is trading at an EV/EBITDA numerous of 17.8x on a TTM foundation. Even so, I feel it is low cost as its small business has been escalating rapidly considering the fact that the appointment of John Loftus as CEO and President in December 2016. Envela closed 2016 with income of $48.3 million, down from $127.9 million in 2012. The net loss, in flip, had widened $1.6 million to $4 million. So, how has the firm managed to get again in the black and surpass its 2012 product sales amount in a interval of less than 5 several years? Very well, it all commenced with slashing SG&A expenditures. And in 2019, Envela bought Echo Environmental and ITAD Usa for $6.9 million from Loftus to develop ECHG. You see, the gross margin of Envela was 17.2% in 2016, but the small business was barely sustainable as SG&A expenditures have been in excess of $10 million for every 12 months. I consider that DGSE continue to isn’t a superior business owing to the rather small margins, and it appears to be that most of the significant improvement in profitability over the

past a few yrs has been coming from the consumer electronics and IT machines segment. I consider that this advancement is probable to continue as it has powerful momentum that even the COVID-19 pandemic could not place an end to it. The company has also designed several bolt-on acquisitions more than the past a number of decades, and CExchange and Avail are the most up-to-date types.

Seeking at the challenges for the bull circumstance, I feel that the important one particular is the sourcing of stock. When Envela stock was at a nutritious stage of $14.6 million as of March 2022, most of that quantity was connected with DGSE. The significant-margin ECHG business experienced inventories of just $2.3 million at the close of Q1 2022.

Envela

1 of the key resources of stock for ECHG is college districts, and it’s attainable that a recession in the United states could direct to reduce training shelling out, which would in transform hurt this company.

Another danger to think about here is that the economical effects of ECHG’s recycling enterprise and DGSE are drastically affected by treasured and other non-ferrous metal costs. If gold and silver charges decline, Envela’s margins will slide.

Investor takeaway

Envela has realized a sizeable turnaround of its small business over the previous couple yrs, and I imagine that the most essential issue for this was the purchase and progress of the large-margin buyer electronics and IT machines ECHG business. This section is rising rapidly, and its margins stay above 40% which is why I view Envela as undervalued at the second. If development fees are sustained, I assume that the firm’s shares really should be investing at something like $9.00 in the in the vicinity of long term.

However, I am worried that inventories at ECHG were at a small amount as of March, and this could lead to difficulties down the road. In see of this, I amount Envela as a speculative invest in.