Is ContextLogic A Good Ecommerce Stock Investment?

alexsl

ContextLogic (NASDAQ:Would like) is an ecommerce business acknowledged for its Desire searching system. The application took off in attractiveness through the height of the pandemic. People today that ended up caught at property embraced Wish’s differentiated “treasure hunt” design and style of discount-shopping for distinctive or unpredicted products.

Due to the fact early 2021, on the other hand, factors have absent painfully incorrect for each ContextLogic as a enterprise and Wish as a inventory. Shares are down far more than 90% from the peak, and the company’s economical outcomes are also a mess. What is gone mistaken for the ecommerce web-site, and is there significantly hope of a turnaround?

Wish Stock Crucial Metrics

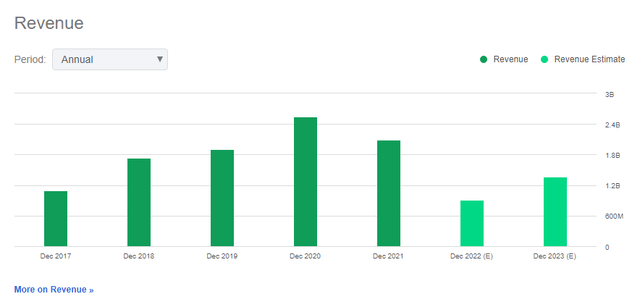

There is certainly 1 critical metric for ContextLogic that must emphasize this firm’s complications correct from the bounce. It can be the company’s top rated-line profits:

Would like revenues (In search of Alpha)

Just after hitting a peak of $2.5 billion in 2020, the firm’s revenues tumbled to $2.1 billion previous 12 months. And then, items acquired definitely negative. For 2022, analysts now anticipate the corporation to generate a mere $907 million of revenues. That’s down by far more than fifty percent versus 2021 and off by in the vicinity of two-thirds because the 2020 peak.

So, let’s be obvious: ContextLogic isn’t really just another ecommerce organization that is seeing a publish-pandemic slowdown. Fairly, ContextLogic is a company that now has a broken enterprise design and requires to wholly reinvent itself if it is going to create shareholder value going forward.

The company’s base line doesn’t glance significantly superior. It really is in no way created a optimistic functioning profits on an once-a-year basis. And, even though the firm has cut fees not long ago, it hasn’t been virtually sufficient to maintain up with plunging revenues. Analysts expect the enterprise to lose 57 cents for each share in 2022, 47 cents in 2023, and deliver an additional 31-cent reduction in 2024.

Offered that the firm’s stock is investing at less than $2/share now, these are alarmingly significant earnings for each share losses that are getting forecast heading forward.

Is ContextLogic Stock Undervalued?

On the foundation of the previously mentioned metrics, I’d argue that ContextLogic stock is overvalued, if anything. The company has generated an functioning loss of at the very least $144 million per year just about every of the previous five several years. From time to time, individuals losses have been significantly bigger, with operations burning by way of a lot more than 50 percent a billion pounds in 2020 on your own.

These substantial losses seemingly have not created a meaningful recurring revenue base or solid brand name that presents the firm some thing to tumble back again on. Despite investing all this capital mostly in promoting, the instant market conditions turned in 2021, WISH’s working results plummeted.

You could argue purely on a marketplace cap basis that shares may possibly be undervalued in just one feeling. The enterprise is nonetheless heading to do all-around a billion in revenues this yr and the market place cap is just hardly over that determine. 1x revenue is not a demanding valuation for an on the web retailer. Or, typically, it would not be. In the case of ContextLogic, nonetheless, these revenues are plunging and you will find little evidence that the company will be equipped to switch by itself close to in the intermediate upcoming.

How Does Want Inventory Evaluate To Other Ecommerce Competitors?

From my comprehending, the large big difference among Would like and larger ecommerce gamers is that Would like has focused on a specialized niche rather than wide-based attractiveness. Compared with, say, Amazon (AMZN), you really don’t go on Want to acquire anything less than the solar. Fairly, Would like has a cut price-procuring driven technique in which persons can buy merchandise that are new, exclusive, or distinct at reasonably priced price details.

This may possibly have tested to be a particularly persuasive possibility through the pandemic when many specialty brick and mortar shops have been shut. In a time when Walmart (WMT) or Costco (Charge) ended up the principal offered in-person procuring activities, purchasing some exciting toy or jewelry item or whatnot from Want gave customers a little something desirable.

Now, nonetheless, Want is competing with a much broader array of alternative searching alternatives. In addition, Wish’s very own reliance on lower price pricing has led to serious worries all over products quality. Numerous critiques cite troubles with items that will not operate for quite lengthy or appear shoddy in design. In went more than that. As fellow Trying to get Alpha writer William Sabga-Aboud pointed out, good quality worries led to France outright blocking the application in that place final fall thanks to items that had been located to be dangerous.

A lot of ecommerce applications have operate into harder functioning conditions among the renewed competitors from physical merchants, source chain challenges, and climbing logistics expenses. It truly is not unreasonable for on the internet marketplaces to be viewing a slowdown in 2022.

But Wish’s decrease in operating metrics is on a full distinct tier from its rivals. This is a firm that desperately requirements a new business technique or internet marketing angle or something to convert matters all around.

Is Wish A Great Lengthy-Expression Investment decision?

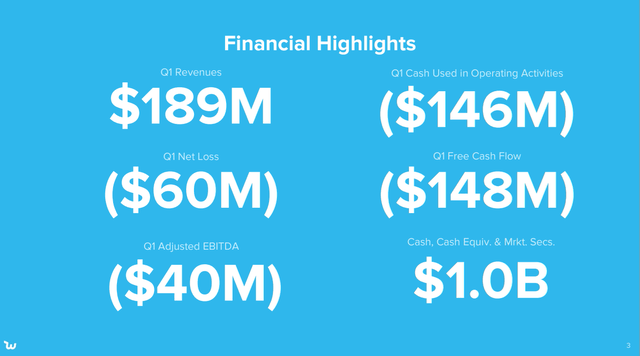

A slide from ContextLogic’s most new quarterly earnings effects puts the company’s predicament into sharp contrast:

Desire economical success (Company presentation)

The a single superior piece of news is that the organization nonetheless has $1. billion of funds and marketable securities left. But, it managed to burn up by means of $148 million of funds just last quarter on your own. Take note that the company’s free hard cash circulation is significantly even worse than its by now sizable net decline and negative adjusted EBITDA.

Dependent just on hard cash by itself, ContextLogic could possibly seem like a decent speculative acquire. Right after all, the industry cap is now $1.1 billion, indicating that the actual running business is only getting valued all around $100 million or so. And, as outlined above, there are continue to once-a-year revenues in the billion greenback assortment as well. That may appear like more than enough to give this a shot at working.

But, at a $150 million quarterly burn off amount, the firm’s dollars is possible to be fatigued by early 2024 if points maintain going as they are at present. In the meantime, any significant turnaround would likely force the organization to change marketing and advertising commit again up or usually spend in expansion initiative. ContextLogic’s initiatives to lower running costs in the latest quarters, as we have observed, have had a devastating impact on the company’s income trajectory.

And, as also famous, it’s a difficult running setting for ecommerce firms and even massive brick and mortar operators like Walmart and Focus on (TGT). ContextLogic is acquiring to check out to execute what would already be a tough company turnaround under unfavorable macroeconomic situations.

Is Want Stock A Invest in, Market, Or Maintain?

ContextLogic has created some improvements. There’s a new CEO. The corporation has enormously rethought its marketing tactic. And it has created some core enhancements in the application, such as acquiring an invite-only approach to onboarding new distributors on the system to enhance high-quality expectations in merchandising.

ContextLogic has been ready to present some tangible indications of progress, this sort of as its web promoter score “NPS” doubling because late 2021. It is a begin.

But you can find however so substantially to be performed. The corporation had 101 million monthly lively people “MAUs” in Q1 of 2021. This collapsed to just 27 million in Q1 of 2022. It truly is difficult to overstate just how immediately or badly this company’s main organization has eroded in latest months.

Combine that with the firm’s substantial cash burn up and the in general predicament right here is grim.

ContextLogic has cash and it nonetheless has a respectable revenue foundation. On the other hand, the odds of the company acquiring again on keep track of seem relatively minimal. The company’s company product has hardly ever continuously developed a financial gain. And now, with its brand tarnished, the business has to check out to carry prospects back all whilst trying to keep fees in examine in the course of a complicated macroeconomic setting.