Our ‘Best Idea,’ Says J.P. Morgan

Significantly has been created of the headwinds the ecommerce section has arrive up versus in the latest instances. Continued supply chain and inflationary pressures amidst slowing purchaser discretionary spending and the impact of the economy’s reopening have all impeded the sector’s progress.

And as was apparent in a disappointing Q1 report, Amazon (AMZN) has felt the pinch much too.

J.P. Morgan’s Doug Anmuth thinks the macro headwinds will nonetheless have a massive portion to engage in in Q2 – notably in the initial 50 percent – nonetheless as comps relieve in the latter half of the yr, and Amazon helps make more headway in “key less than-penetrated categories” this sort of as grocery, CPG, clothing & equipment, & home furnishings/appliances/machines, revenue progress should also choose up steam in 2H22.

There is also another component to take into consideration when analyzing Amazon’s around-time period potential clients. The organization has invested intensely about the previous few of a long time the workforce has almost doubled to 1.6 million, although the achievement community is now 2 times as big. But the corporation now appears to have also much potential – both equally in the workforce and infrastructure intelligent.

That said, Amazon has presently claimed this year’s achievement capex would be reduced than last 12 months, when transport capex must also arrive in “flat to a little down.” The result need to be an all round reduction of ~55% of the total capex spend in contrast to very last calendar year.

The slowdown in paying really should also show helpful to OI margins, which Anmuth expects will increase as the calendar year progresses.

“Macro elements will take extended to enjoy out,” extra the 5-star analyst, “but the firm has raised Primary prices & released a fuel surcharge to offset, & we hope AMZN to improve into its upfront paying far more in 2H22.”

In other places, AWS observed out Q1 with a backlog of $88.9 billion – its most important at any time – when advancement accelerated to 68% yr-in excess of-year. Anmuth thinks 30%+ AWS earnings growth is “sustainable” in 2022, and as comps ease, Advertising need to also see a substantial uptick.

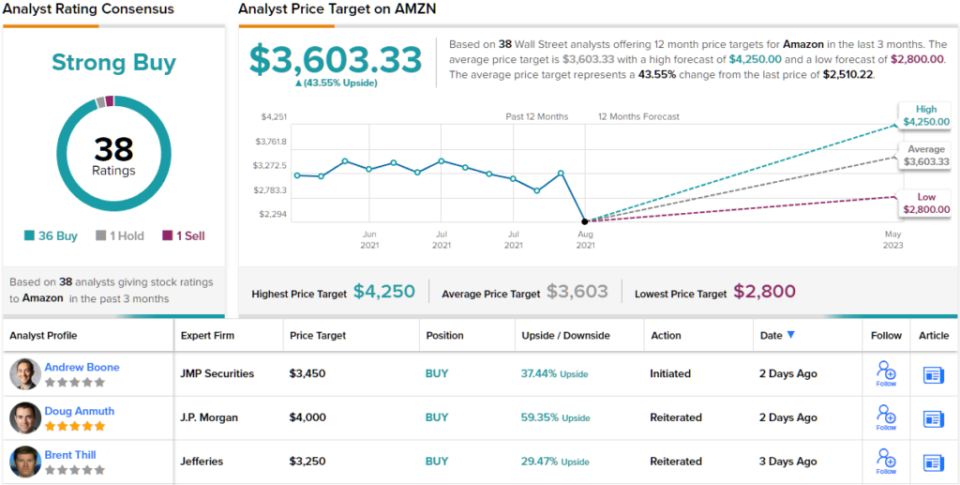

All in all, Anmuth phone calls Amazon his “Best Plan,” and reiterated an Obese (i.e., Invest in) rating alongside with a $4,000 cost goal. The implication for investors? Upside of 59%. (To check out Anmuth’s monitor report, click in this article)

The Street’s cadre of analysts nearly unanimously concur of the 38 reviews on file, 36 are to Get, generating the consensus view on this inventory a Sturdy Acquire. Heading by the typical focus on of $3,603 and alter, shares are predicted to climb ~44% bigger in the year ahead. (See Amazon inventory forecast on TipRanks)

To find very good thoughts for shares investing at desirable valuations, check out TipRanks’ Greatest Shares to Acquire, a newly introduced software that unites all of TipRanks’ equity insights.

Disclaimer: The views expressed in this short article are exclusively those people of the highlighted analyst. The information is meant to be used for informational reasons only. It is very vital to do your very own assessment right before generating any investment decision.